Eagle Energy Trust announced that they have entered into an agreement to acquire a 92.5% interest in 3,175 gross (2,937 net) acres of land near Midland. The purchase price is $113.4 million which equals a transaction price of $38,600/acre!

The asset includes 600 boe/d of production as of March and the company expects production to be approximately 1,000 boe/d by the end of 2012 (sound familiar...) Estimated proved plus probable reserves is approximately 10.2 mmboe.

"These long life, high netback assets represent a solid, low risk entry-point for Eagle into one of the most prolific and well-established oil weighted basins in North America. We believe that the Permian Basin will form a new strong core area of future operations for Eagle. It is one of North America's most productive oil-weighted basins and has demonstrated, on a recurring basis, the addition of new reserves horizons and enhanced exploitation of existing horizons in the multi-zone stacked pay resource," says Richard Clark, President and CEO of Eagle Energy Trust.

As a comparison, on April 4 Lynden Energy Corporation announced over 500 boe/d after royalty net production and has estimated end of 2012 production of approximately 1,000 boe/d. Most of this production is located within their West Martin and Wind Farms Wolfberry projects where Lynden owns 3,841 net acres and has 9.8 mmboe of proved plus probable reserves as of 6/30/11. The Eagle Energy Trust asset acquisition has very similar numbers to Lynden's West Martin and Wind Farms projects. Should one value Lynden's West Martin and Wind Farms acreage on a similar acreage metric as the Eagle Energy transaction, those lands alone would be valued at approximately $148 million which far exceeds the company's current market cap. After adding in Lynden's Tubb and Mitchell Ranch acreage, one can conclude that Lynden has incredible potential.

Monday, April 30, 2012

Horizontal Wolfcamp article, etc.

There was a nice article on the Horizontal Wolfcamp published by Oil and Gas Investor magazine. It's worthwhile reading for those interested. Here is a link to the article which is located on Approach Resources website: "Horizontal Wolfcamp"

Also, Energen released their Q1 2012 results last week. Here are a couple of comments from James T. McManus, II, the company's Chairman and CEO:

"As you know there is growing excitement about the horizontal Wolfcamp and Cline potential in the Midland Basin. We currently are participating as a non-operated partner with Laredo in the horizontal Wolfcamp well near our Glasscock County acreage, the early results are encouraging and we’re pleased to be getting some data points that will help us to better assess the potential on our acreage."

"We also are closely monitoring Cline activity in the Midland Basin, obviously, a success of either this plays on our acreage could impact our future drilling plant in the Midland Basin."

Here is the link to the transcript as posted on Seeking Alpha: "Energen Earnings Call transcript"

Also, Energen released their Q1 2012 results last week. Here are a couple of comments from James T. McManus, II, the company's Chairman and CEO:

"As you know there is growing excitement about the horizontal Wolfcamp and Cline potential in the Midland Basin. We currently are participating as a non-operated partner with Laredo in the horizontal Wolfcamp well near our Glasscock County acreage, the early results are encouraging and we’re pleased to be getting some data points that will help us to better assess the potential on our acreage."

"We also are closely monitoring Cline activity in the Midland Basin, obviously, a success of either this plays on our acreage could impact our future drilling plant in the Midland Basin."

Here is the link to the transcript as posted on Seeking Alpha: "Energen Earnings Call transcript"

Friday, April 20, 2012

Another article on the Cline Shale

An article was written on the Cline shale by Nissa Darbonne. Here are a couple of quotes from it:

"Laredo Petroleum Inc. chairman and chief executive officer Randy Foutch says the Cline shale 'is a world-class shale'."

"The Cline is less known (but) we know a lot about it,” Foutch says. Across at least 80 miles in the Midland Basin, the formation is fairly unchanging north to south, he adds."

"Laredo Petroleum Inc. chairman and chief executive officer Randy Foutch says the Cline shale 'is a world-class shale'."

"The Cline is less known (but) we know a lot about it,” Foutch says. Across at least 80 miles in the Midland Basin, the formation is fairly unchanging north to south, he adds."

Thursday, April 19, 2012

Cline Shale Generating Industry Buzz! Lynden Poised to Benefit

One theme became clear for those who attended Howard Weil 2012, one of the premier investor energy conferences. The Cline shale is generating significant industry buzz! From Concho Resources to Devon Energy to Pioneer Natural Resources, the message was focused on the Cline shale and its vast potential. Companies are finding out that below the Wolfcamp lies this highly prospective zone. They are also discovering that the Wolfcamp (some companies are now grouping the Cline together with the Wolfcamp and referring to both zones as the Wolfcamp) is much more extensive, potentially spanning the entire Basin. Because large Wolfcamp acreage parcels are hard to come by, the play is on the verge of a breakout where companies will have to buy out smaller independents in order to establish a sizeable position.

How to Play the Cline

Many companies are active in the Permian Basin. Pioneer, Devon, Apache, EOG, Chesapeake, Range and Concho all have positions in the Midland Basin and the Wolfcamp. These companies have market caps ranging from $8.8 billion to $36.0 billion. Although these companies should experience an uptick with Wolfcamp success, another company could see multiples of its existing share price.

Lynden Energy Corp. has successful positions in the Wolfberry located at their West Martin project in Martin County and Wind Farms project in Glasscock County. In fact, their current reserves are primarily assigned to just these two areas. Valuations based on these two areas alone would warrant a higher share price.

On April 4, Lynden announced the continued success of their Tubb A #1 well. This well has continued to produce oil in excess of 100 barrels per day over the past 90 days since it was tied in. Should this prospect area ultimately be proven out it would support a significantly higher share price. On 40 acre spacing, there are potentially 170 gross locations with the next well to spud later this month and several more prior to year end.

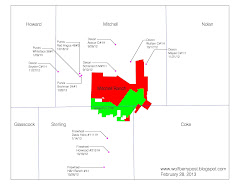

We believe that Lynden is considerably undervalued based on their Wolfberry holdings at West Martin, Wind Farms and Tubb. Now, how does this relate to the Cline? Lynden has an interest in 103,400 net acres at an area on the border of Sterling and Mitchell Counties called Mitchell Ranch. The market hasn’t yet assigned value to this land. Land around Mitchell Ranch is becoming scarce and exploration of the Wolfcamp shale is developing around the area. Although Chesapeake, Lynden’s farmout partner on the property, is currently only exploring the Mississippian zones below the Wolfcamp at Mitchell Ranch, it is likely that the Cline shale exists throughout their acreage. In fact, Mitchell Ranch is located near the center of the extent of the Cline shale as depicted on a map prepared by Devon Energy in their latest presentation!

Lynden’s net position at Mitchell Ranch amounts to approximately 34,150 acres. As we know based upon recent Wolfberry land sales, successful Wolfberry acreage can sell for as much as $35,000 per acre or more. Should the Cline shale ultimately become a viable source of oil as the industry is starting to believe, Mitchell Ranch could become extremely desirable. Could the acreage ultimately be worth $5,000/acre, $10,000/acre or more? We believe so!

This is where Lynden becomes extremely interesting. At even just $5,000/acre, Lynden is sitting on a very valuable asset. Their 34,150 acres valued at $5,000/acre translates to $170 million. At $10,000/acre this value becomes $340 million. Together with their Wolfberry holdings, Lynden could be a company worth $400 million or more. Given Lynden’s current market cap, this stock has room to run.

It’s easy to see why we are so excited about this company’s prospects. Because Lynden continues to have success in the Wolfberry, the downside risk here is limited. The upside associated with Tubb and Mitchell Ranch is tremendous! Like we have mentioned previously, “Buying Lynden at its current valuation could be looked upon as buying their Tubb and Mitchell Ranch projects for free and Lynden could be a stock worth several dollars per share!”

How to Play the Cline

Many companies are active in the Permian Basin. Pioneer, Devon, Apache, EOG, Chesapeake, Range and Concho all have positions in the Midland Basin and the Wolfcamp. These companies have market caps ranging from $8.8 billion to $36.0 billion. Although these companies should experience an uptick with Wolfcamp success, another company could see multiples of its existing share price.

Lynden Energy Corp. has successful positions in the Wolfberry located at their West Martin project in Martin County and Wind Farms project in Glasscock County. In fact, their current reserves are primarily assigned to just these two areas. Valuations based on these two areas alone would warrant a higher share price.

On April 4, Lynden announced the continued success of their Tubb A #1 well. This well has continued to produce oil in excess of 100 barrels per day over the past 90 days since it was tied in. Should this prospect area ultimately be proven out it would support a significantly higher share price. On 40 acre spacing, there are potentially 170 gross locations with the next well to spud later this month and several more prior to year end.

We believe that Lynden is considerably undervalued based on their Wolfberry holdings at West Martin, Wind Farms and Tubb. Now, how does this relate to the Cline? Lynden has an interest in 103,400 net acres at an area on the border of Sterling and Mitchell Counties called Mitchell Ranch. The market hasn’t yet assigned value to this land. Land around Mitchell Ranch is becoming scarce and exploration of the Wolfcamp shale is developing around the area. Although Chesapeake, Lynden’s farmout partner on the property, is currently only exploring the Mississippian zones below the Wolfcamp at Mitchell Ranch, it is likely that the Cline shale exists throughout their acreage. In fact, Mitchell Ranch is located near the center of the extent of the Cline shale as depicted on a map prepared by Devon Energy in their latest presentation!

Lynden’s net position at Mitchell Ranch amounts to approximately 34,150 acres. As we know based upon recent Wolfberry land sales, successful Wolfberry acreage can sell for as much as $35,000 per acre or more. Should the Cline shale ultimately become a viable source of oil as the industry is starting to believe, Mitchell Ranch could become extremely desirable. Could the acreage ultimately be worth $5,000/acre, $10,000/acre or more? We believe so!

This is where Lynden becomes extremely interesting. At even just $5,000/acre, Lynden is sitting on a very valuable asset. Their 34,150 acres valued at $5,000/acre translates to $170 million. At $10,000/acre this value becomes $340 million. Together with their Wolfberry holdings, Lynden could be a company worth $400 million or more. Given Lynden’s current market cap, this stock has room to run.

It’s easy to see why we are so excited about this company’s prospects. Because Lynden continues to have success in the Wolfberry, the downside risk here is limited. The upside associated with Tubb and Mitchell Ranch is tremendous! Like we have mentioned previously, “Buying Lynden at its current valuation could be looked upon as buying their Tubb and Mitchell Ranch projects for free and Lynden could be a stock worth several dollars per share!”

Tuesday, April 17, 2012

Article about Devon and the Cline Shale

An article posted on Seeking Alpha talks about Devon exploiting the Cline shale. "Devon has chosen to gain access in another region, exploiting the midland

section of the Basin in the Cline formation." The article further states, "With Devon's setting aside of capital money to continually acquire land, its diversified portfolio, focus on oil, healthy

balance sheet, and smart management plays make for a good combined package for a

long-term energy company."

Lynden Energy's non-brokered Private Placement

As much as

another private placement dilutes the company, we are very excited and view

this as a positive. The ability to add

funds and ensure the longevity of the company means that Lynden Energy Corp.

will not fall into financial jeopardy.

Given that financing is difficult to obtain in this market, Lynden will achieve

a milestone by obtaining $6.3 million should the placement close fully

subscribed. It appears the company’s

borrowing base is not accelerating as fast as their drilling but the financing

allows some breathing room.

As the volume

today shows, the market is clearly supporting the financing. There are buyers out there who like the story

and buying large blocks. The buyers in

the market and those who participated in the financing have apparently completed

their due diligence and like what they see.

We view

Lynden’s prospects as better than before the private placement was

announced. Surely, the dilution is not

something we were looking forward to but this was anticipated given the rapid

pace of development. The company’s

financial future is now ensured until their borrowing base increases. With support being shown in today’s market and the industry buzz and excitement about the Cline shale,

we believe that Lynden can realize its market cap potential and that this stock

can return multiples.

Wednesday, April 4, 2012

Lynden releases production numbers and comment about Howard Weil 2012

Lynden Energy Corp. reported production after royalties of over 500 boepd on average over a ten day period ending March 31. Highest daily production during the period was 595 boepd! These are excellent numbers demonstrating continuing high production from their Tubb A #1 well as well as shallow declines from their existing wells.

Of significance is that the Tubb A #1 well is still producing over 100 barrels of oil per day. This number does not include natural gas or natural gas liquids and is 90 days after being tied in. Should these numbers be replicated, Lynden has some very special acreage. The Tubb Prospect Area includes 7,341 gross acres of which Lynden's net interest is approximately 2,469 net acres. Additional success here will surely capture industry attention and Lynden's large acreage puts them in a nice position to capitalize.

Recently, Richard Mason wrote an article about Howard Weil 2012. The article titled "Operators Hint at Two New Liquids Plays, Major Permian Discovery" is one more leg to Lynden's story. The apparent industry excitement about the Cline shale is generating a lot of buzz. Devon, Concho, EOG and Pioneer are all actively pursuing the Cline shale. "Pioneer and Concho are now suggesting that the prospective Wolfcamp (Cline) spans the entire Midland basin," the article states. (For those unfamiliar with the Cline shale, it exists just below the Wolfcamp shale zones. Some companies are grouping the shales together and calling them the Wolfcamp shale.)

Tim Leach, CEO of Concho Resources, commented that they have 45,000 net acres of new holdings and their primary target is the Cline shale. "The punchline here is we think this play in the northern part of the Midland Basin will be very similar in returns and composition to the Wolfcamp in the southern part of the Midland Basin."

A couple of additional comments from the article. "Long story short: the horizontal Wolfcamp is on the verge of a substantial breakout in the Permian Bains." Also, Scott Sheffield, CEO of Pioneer, states "People... will will have to buy out smaller independents. It will be really tough to get a large acreage position because most land is held by production by the various operators." Again, Lynden is in an excellent position, because of their 103,400 acre Mitchell Ranch project. The next few months will be very interesting...

Of significance is that the Tubb A #1 well is still producing over 100 barrels of oil per day. This number does not include natural gas or natural gas liquids and is 90 days after being tied in. Should these numbers be replicated, Lynden has some very special acreage. The Tubb Prospect Area includes 7,341 gross acres of which Lynden's net interest is approximately 2,469 net acres. Additional success here will surely capture industry attention and Lynden's large acreage puts them in a nice position to capitalize.

Recently, Richard Mason wrote an article about Howard Weil 2012. The article titled "Operators Hint at Two New Liquids Plays, Major Permian Discovery" is one more leg to Lynden's story. The apparent industry excitement about the Cline shale is generating a lot of buzz. Devon, Concho, EOG and Pioneer are all actively pursuing the Cline shale. "Pioneer and Concho are now suggesting that the prospective Wolfcamp (Cline) spans the entire Midland basin," the article states. (For those unfamiliar with the Cline shale, it exists just below the Wolfcamp shale zones. Some companies are grouping the shales together and calling them the Wolfcamp shale.)

Tim Leach, CEO of Concho Resources, commented that they have 45,000 net acres of new holdings and their primary target is the Cline shale. "The punchline here is we think this play in the northern part of the Midland Basin will be very similar in returns and composition to the Wolfcamp in the southern part of the Midland Basin."

A couple of additional comments from the article. "Long story short: the horizontal Wolfcamp is on the verge of a substantial breakout in the Permian Bains." Also, Scott Sheffield, CEO of Pioneer, states "People... will will have to buy out smaller independents. It will be really tough to get a large acreage position because most land is held by production by the various operators." Again, Lynden is in an excellent position, because of their 103,400 acre Mitchell Ranch project. The next few months will be very interesting...

Subscribe to:

Posts (Atom)