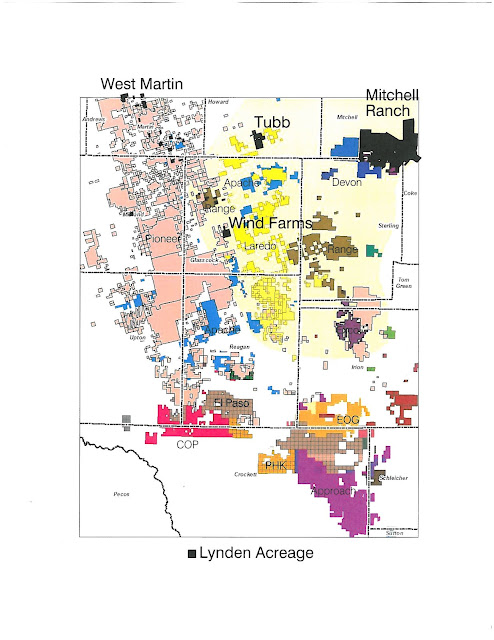

Yesterday’s announcement by Lynden Energy Corp. of a

sale of certain assets to BreitBurn Energy Partners provides a basis for

valuation of Lynden‘s remaining lands. (LINK TO PRESS RELEASE)

We believe the sale was likely located within the

West Martin project area. The $25

million sale price for 630 net acres equates to a land valuation in West Martin

at $40k/acre. Using this transaction as

a benchmark, it is possible to project values for Lynden’s remaining lands, and

in turn, a reasonable market cap/fully diluted share price for LVL.

First, our assessment is that Lynden’s Wind Farms

project is every bit as valuable (if not more) as the land included in

yesterday’s announcement. The BreitBurn

sale thus provides a justifiable comparable for the Wind Farms land at

$40k/acre.

Lynden’s Tubb project is located in an area that in

general is not as developed/proven as the West Martin and Wind Farms. That said, the Tubb project area is in the

heart of the developing Fusselman play.

The Fusselman Shale is located below the Mississippian Shale and is

being explored by Cobra, Target, Trilogy and others. Cobra’s Fusselman well is located adjacent to

Lynden’s Tubb project and is rumored to be very successful. Apache is developing the Fusselman and the Cline just south of Tubb and immediately east of Wind Farms. We believe that a reasonable valuation for

Lynden’s Tubb land is $20k/acre based on its Wolfberry exposure. Further, the

value of these lands could increase to as much as $40k/acre with successful

Fusselman and Cline drilling by other companies.

The drilling by Devon adjacent to the northern

border of Mitchell Ranch and the Firewheel well (rumored to be of substantial

size) to the south leads one to believe that a valuation of Lynden’s Mitchell

Ranch lands at $2k/acre is very low. A

valuation of $7.5k to $10/acre is entirely reasonable, given the current

desirability of Cline Shale land.

From an operational viewpoint, the BreitBurn deal provides

Lynden with plenty of working capital in exchange for a relatively small portion

of its total assets (less than ten percent of its Wolfberry land). The $25

million proceeds (net to Lynden) provide a solid cash cushion for the Company, greatly

minimizing any worries about future financings or Lynden’s ability to continue

as a viable company for the foreseeable future.

What does this mean?

Lynden’s remaining Wolfberry acreage in aggregate can be valued at $200 to

$250 million: this asset alone would equate to twice the Company’s current market cap. Adding in the potential of Mitchell Ranch, the

sum of Lynden’s assets could easily reach $500 to $600 million, translating to

a fully-diluted price of up to $4/share.

Is this possible?

With the frenzy to acquire land in the Wolfberry and Cline and the

validation of present Lynden holdings based on the BreitBurn sale, we believe

so. In January 2011, The Oil and Gas

Investments Bulletin called Lynden Energy a “No Brainer.” That comment now looks accurate and we believe

that Lynden Energy Corp. is indeed a “No Brainer.”